Many companies offer life insurance as a benefit to their employees. Some provide a certain amount for free, often one times salary, with the option to purchase more. Simply check the box, pick your coverage amount and the appropriate premium will be deducted from your check. It couldn’t be easier! And since you are part of a group you must be getting a group discount as well, right? Wrong! In fact, group term insurance could cost you tens of thousands of dollars more than individual term insurance over time! There are two reasons for this: lack of medical underwriting and price increases every 5 years.

The lack of medical underwriting means there is no physical required to get the insurance. Granted this makes things easy for you but insurance companies know not everyone is in good health and price accordingly. The premiums typically average below the standard rates of medically underwritten policies. Simply put, if you are in good health, you could save thousands of dollars by taking advantage of good health discounts available on individual policies.

The second issue, price increases every 5 years, really becomes problematic over the age of 40. Any HR department can provide a chart of premiums usually expressed per $1000 of coverage per pay period. The chart will be broken down by age brackets 20-24, 25-29, 30-34, 35-39, etc. Pay close attention to how much they increase from 40-65. What started out as just a few bucks out of your paycheck quickly becomes extremely expensive term insurance. Individual term policies can be guaranteed to remain the same price for even up to 30 years.

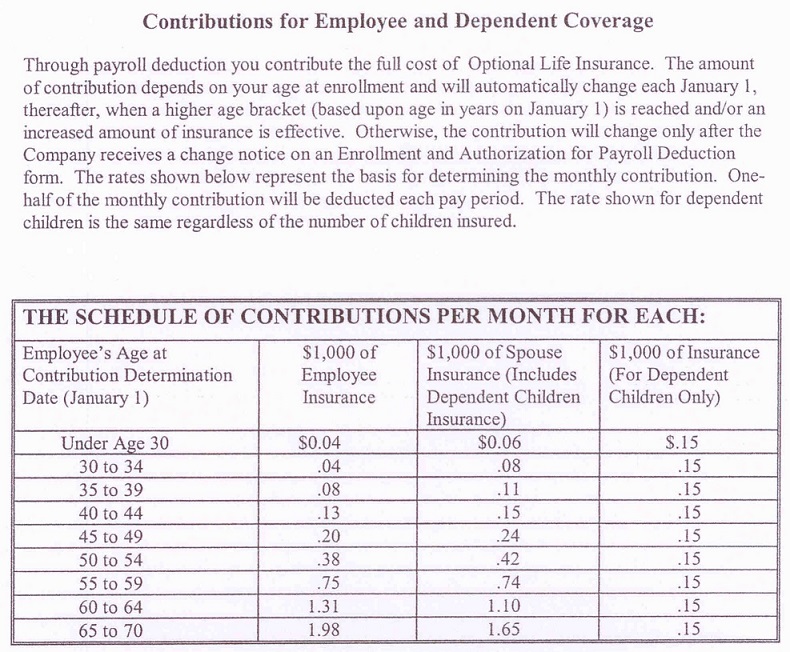

To explain, let’s look at an actual chart detailing insurances offered to employees of a large company.

Referencing the above chart, let’s use the example of a 35 year old male in good health that wants $500,000 in coverage.

| Age at contribution date | Contribution | Total for 5 years | |

| 35-39 | .08 x 500 x 12 = $ 480/yr | $2,400 | |

| 40-44 | .13 x 500 x 12 = $ 780/yr | $3,900 | |

| 45-49 | .20 x 500 x 12 = $ 1,200/yr | $6,000 | |

| 50-54 | .38 x 500 x 12 = $ 2,280/yr | $11,400 | |

| 55-59 | .75 x 500 x 12 = $ 4,500/yr | $22,500 | |

| 60-64 | 1.31 x 500 x 12 = $ 7,860/yr | $39,300 | |

| Total for 30 years of premium | $85,500 | ||

Now let’s compare that to purchasing a 30 year term policy outside of work. $500,000 in coverage for a 35 year old male in good health would cost $460 a year, with a rate guaranteed for 30 years. The total premium paid over 30 years would be $13,800. That’s a savings of $71,700!

By switching to individual term insurance, you could save thousands of dollars in premiums and lock in those premiums for the length of time you chose. Plus, your insurance is no longer tied to your employer in case you quit your job or the company discontinues offering the benefit. If you are currently paying for life insurance through your employer, I highly encourage you to contact your HR department and get the chart, then contact our office to see how much you could be saving.